When you lease a vehicle, you’re making a smart choice to drive a newer car without the long-term commitment of buying. But have you thought about what happens if your leased car is stolen or totaled in an accident?

That’s where gap insurance for leased vehicles comes in. It’s a safety net that covers the difference between what you owe on your lease and what your insurance company pays if your car’s total loss payout falls short. Without it, you could be left paying out of pocket for a car you no longer have.

You’ll discover why gap insurance matters, how it works with leased vehicles, and whether it’s the right move for you. Keep reading to protect your wallet and drive with peace of mind.

Gap Insurance Basics

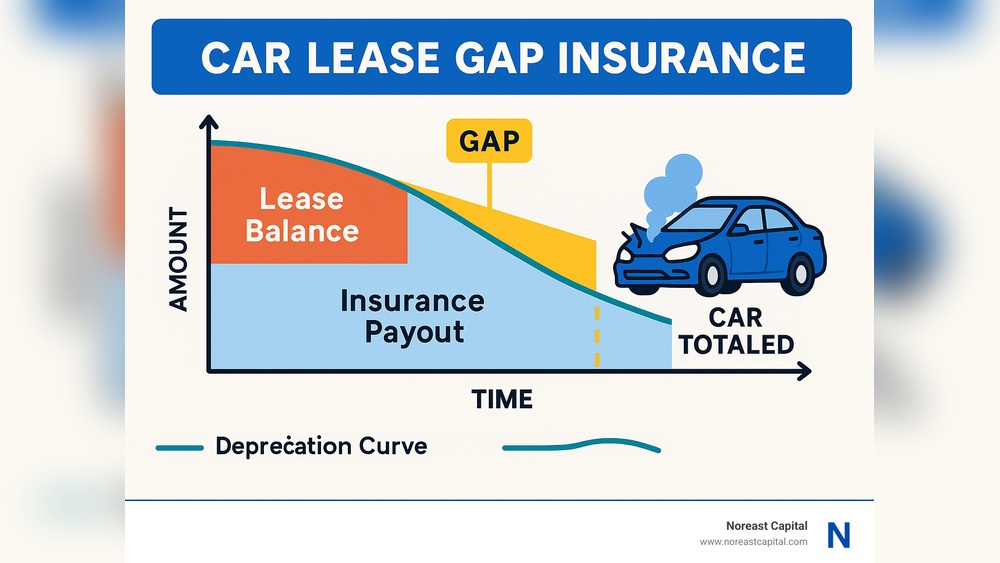

Gap insurance helps cover the difference between what your car is worth and what you owe on it. This is important if your leased vehicle is stolen or damaged beyond repair. The insurance pays the “gap” so you don’t have to pay out of pocket.

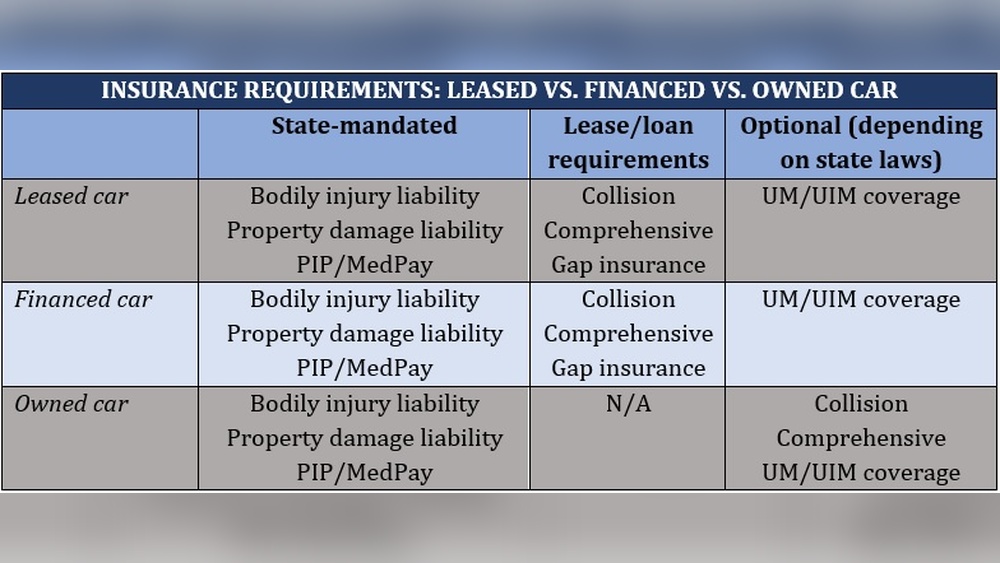

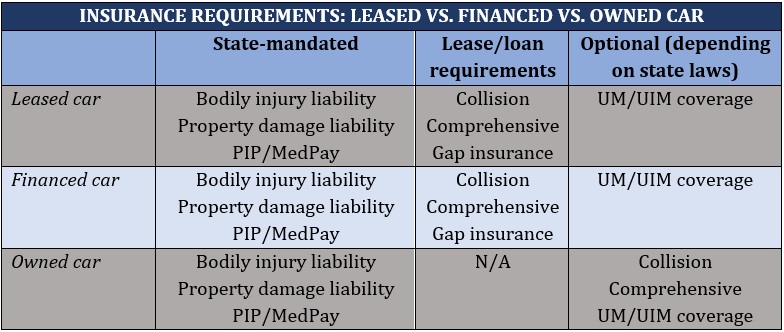

For leased vehicles, gap insurance works by covering the remaining lease payments or loan balance. It protects you from owing more than the car’s value after an accident or theft. Many leases require gap insurance or include it in the contract.

| Gap Insurance | Collision Coverage |

|---|---|

| Covers difference between car value and lease balance | Covers repair costs after a collision |

| Protects against financial loss if car is totaled or stolen | Protects vehicle damage regardless of who caused it |

| Usually required for leased cars | Optional but recommended for all drivers |

Importance Of Gap Insurance For Leased Vehicles

Leased vehicles lose value quickly after purchase. This is called depreciation. The amount you owe on your lease may be more than the car’s current value. Without gap insurance, you risk paying the full lease balance if the car is lost or damaged.

Financial risks arise if the car is stolen or totaled. Your regular insurance only pays the car’s market value, not what you owe. Gap insurance covers the difference, so you don’t pay out of pocket.

| Scenario | How Gap Insurance Helps |

|---|---|

| Accident causes total loss | Covers the lease balance beyond insurance payout |

| Car theft | Pays off the remaining lease amount |

| Severe damage repair costs exceed value | Protects from paying the full lease payoff |

Lease Agreements And Gap Insurance

Gap insurance protects you if your leased car is stolen or totaled. It pays the difference between your car’s actual cash value (ACV) and what you still owe on the lease. This coverage helps avoid paying out of pocket for the remaining lease balance.

Check your lease contract carefully. Some leases already include gap insurance. If it does, you won’t need to buy extra coverage. If it doesn’t, you might want to consider adding it.

Many car dealerships include gap insurance in the lease price. Ask your dealer if gap insurance is part of the lease. This can save you time and money.

Cost And Coverage Options

Gap insurance for leased vehicles usually costs between $300 and $700 per year. The price depends on the car’s value and lease length. Some dealers include gap insurance in the lease contract, but this can make the lease more expensive. Buying gap insurance from an insurer often costs less and offers more flexible options.

| Source | Advantages | Disadvantages |

|---|---|---|

| Dealer | Convenient, included in lease payments | Usually more expensive, less flexible |

| Insurer | Lower cost, customizable coverage | Separate policy, requires extra effort |

Alternatives to gap insurance include:

- Paying extra down payment to reduce loan balance

- Choosing a lease with lower depreciation

- Using savings to cover any potential loss

Pros And Cons Of Gap Insurance

Gap insurance helps cover the difference between your car’s value and what you owe on your lease. It protects you if your vehicle is stolen or totaled. Many lease holders find this coverage useful because lease contracts often require it or include it automatically.

Benefits for lease holders include peace of mind and financial protection. Without gap insurance, you might have to pay out of pocket for the remaining lease balance. It also helps avoid large unexpected expenses after an accident.

Potential downsides include added monthly costs for the insurance. Some people might already have gap coverage through their lease, making extra insurance unnecessary. Always check your lease agreement first.

Impact on down payments can be negative. Putting a large down payment on a leased car might not be wise. If the car is totaled early, you could lose that down payment due to negative equity.

How To Get Gap Insurance

Adding gap insurance to your lease is often the easiest option. Many dealerships include it in your lease contract. This way, the cost is part of your monthly payment. Always read your lease agreement carefully to see if gap insurance is already included. If not, ask the dealer if you can add it before signing.

Buying gap insurance separately is another choice. You can purchase a policy from an insurance company. This option gives you more flexibility to shop around. Keep proof of your policy handy to show your leasing company if needed.

| Tips for Comparing Policies |

|---|

| Check if the policy covers total loss and theft. |

| Compare monthly costs and coverage limits. |

| Look for any exclusions or hidden fees. |

| See if the policy works with your primary insurance. |

| Read customer reviews for reliability and service. |

Claims And Payout Process

Filing a Gap insurance claim starts with notifying your insurance company. Provide all necessary documents like the police report and lease agreement. The insurer will review your claim and contact the leasing company.

During a total loss, the insurance pays the actual cash value (ACV) of the vehicle. Gap insurance covers the remaining lease balance not covered by ACV. This helps avoid paying out-of-pocket for a totaled car.

| Common Claim Issues | Details |

|---|---|

| Missing Documents | Delays happen if lease papers or police reports are missing. |

| Lease Terms | Some leases may exclude certain losses or damages. |

| Claim Timing | Late claims can lead to rejection or reduced payouts. |

Frequently Asked Questions

Should I Get Gap Insurance On A Leased Vehicle?

Gap insurance on a leased vehicle covers the difference between its actual cash value and your lease balance if totaled or stolen. Many leases require it, and it protects you from owing more than the car’s worth. Review your lease agreement to check if gap insurance is included.

Do I Need Gap Insurance On A Lease Car?

Gap insurance is not required on a lease car but protects you if the vehicle is totaled or stolen. It covers the difference between the car’s value and what you owe. Check your lease agreement to see if gap insurance is included before purchasing separately.

What Is The 1.5 Rule When Leasing A Car?

The 1. 5 rule in car leasing means your lease payments should not exceed 1. 5% of the car’s MSRP monthly.

Does A Lease Automatically Have Gap Insurance?

A lease does not automatically include gap insurance. Check your lease agreement to confirm if gap coverage is provided or purchase it separately.

Conclusion

Gap insurance protects you from owing more than your leased car’s value. It covers the difference if your vehicle is totaled or stolen. Many leases include gap coverage, but check your agreement carefully. Having gap insurance can save money and stress after an accident.

It is a smart choice for peace of mind. Always review your lease and insurance options before deciding. This simple step helps protect your finances during your lease term.

Read More:

- Car Warranty Claim Process: Essential Steps to Maximize Your Coverage

- Electric Vehicle Lease Deals: Unbeatable Offers You Can’t Miss

- Mechanical Breakdown Insurance Quote: Save Big with Expert Tips

- Low Risk Driver Insurance Rates: Save Big with Smart Coverage

- Rear End Collision Settlement: Maximize Your Compensation Today

- Drunk Driver Accident Compensation: Maximize Your Claim Today

- No Deposit Auto Insurance Plans: Save Big with Zero Upfront Fees

- Car Lease Insurance Requirements: Essential Coverage Tips You Need